August 2017 — By John Mathis

In this article, we focus on a specialized market niche of collateral valuation and appraisals – a small but important part of the ecosystem in the underwriting process. We highlight the most recent M&A transactions, the key players and comments from leading Appraisal Management Companies (AMC) on how Fannie & Freddie (GSEs) are impacting the industry. From our point of view in the coming year – watch for more consolidation among AMC players as scale wins, GSEs disruption likely accelerates this trend while structural limitations to pricing (borrower fees) will continue to restrict industry profitability.

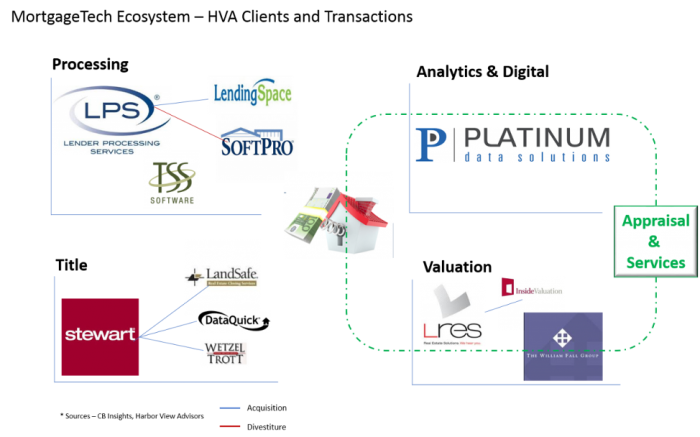

One of the areas of focus for my firm is a not-so-little corner of the FinTech world we think of as MortgageTech. There are many players and many ways to slice up service providers to the $14 trillion mortgage market. As we noted last year, following the annual Mortgage Bankers Association conference, Mortgage Tech is going through an innovation surge. The drivers seemed poised to continue this year with smaller lenders willing to experiment with new technology, a more steady purchase market and continued trends in e-mortgage/digital disruption.

The MortgageTech and Appraisal/Valuation Services markets have seen a tremendous shift in the past few years as key players have consolidated while others have fortified their positions through nearly a billion dollars in acquisitions at notable valuations, averaging well over 2X Revenue:

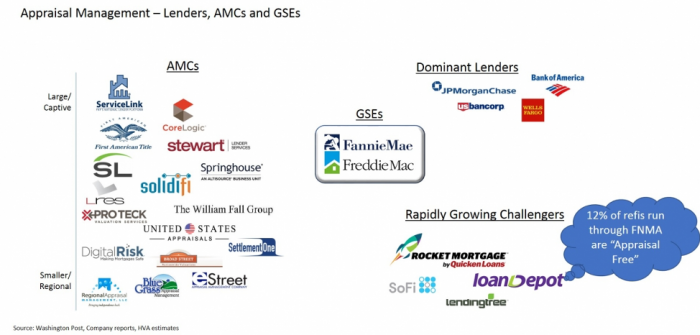

At the highest level, there are three key groups of players in the valuation market: Lenders, Appraisal service providers (AMCs, software, analytics etc) and the GSEs (Freddie & Fannie). The elephant in the market are the GSEs (Government Sponsored Enterprise: e.g. Freddie & Fannie) which have apparently recovered from the housing crisis and notably, are conducting their own disruptive initiatives aimed at a more efficient property valuation process. The extent of “Appraisal Waivers” or “Appraisal-free mortgages” and other requirements for presenting loans to Freddie and Fannie continue to be a topic of discussion for most of the industry players. Notably, one non-bank lender indicated that up to 12% of its Fannie submissions are “Appraisal-Free”.

Additionally, GSE reform is likely to become a headline for next year – potentially further “spooking” the AMC ecosystem (see “Treasury Secretary Mnuchin: Fannie, Freddie reform is a 2018 issue”, Appraisal Institute, HousingWire, 9/15/2017).

As this GSE disruption is such a current topic, we thought it would be helpful to survey our network of clients and confidants to gather their take on the likely impact from Fannie and Freddie shifting more towards “appraisal-free mortgages”. While not a statistical survey by any stretch, the anecdotal commentary is telling:

AMC technology provider: “I can’t count how many times I have heard appraisers will soon become obsolete. Based on the lenders I have talked to; these automated valuation programs are only eligible for a very small subset of borrowers (the perfect borrower and collateral).”

AMC: “…both Freddie and Fannie are experimenting – Fannie just doesn’t put out as many press releases. I’m hearing directly that they can cover materially more than the 50% of appraisal needs they are quoting (massive database). Everyone is thinking it’s only for ReFi – but it is very likely to move into Purchase.”

Industry Analyst: “… they are looking for ways to streamline the process for the perfect borrower/collateral, which they have really already been doing with appraisal waivers from Fannie’s Desktop Underwriter for years. However, government loans (FHA/VA) will always require some type of appraisal as they have to understand the condition of the asset to collateralize the loan.”

AMC: “Note, they are officially using automated valuations NOW for BOTH refinance and origination. Only thing that could change the course of this disintermediation is a market interruption (or FHSA says too risky…)”

Software provider: “This action, along with Fannie’s PIW which will soon make its way to originations, will remove about 10% of the appraisal volume from the market within 5 years. Right now the regulators are limiting the amount of volume the GSE’s can route through programs like this to 5%.“

AMC: “More small or weak AMC closings likely – Finiti, AppraiserLoft…”

AMC technology provider: “I believe big data will be levered more in the valuation process, but I do not think it will replace the appraiser in its entirety. Your typical borrower (with a higher debt to income ratio, which is most common) will never qualify for these types of programs, resulting in an appraisal being required.”

In Summary

While these comments are obviously speculative, and some are even contradictory, there does seem to be a consensus that change is coming. Some degree of disruption seems inevitable given a large government entity, high concentrated lender market and restrictive regulatory conditions and an inflexible industry fee model. As compliance costs and/or risks rise, we would expect to see further AMC consolidation as scale solutions are most likely to survive.

DISCLAIMER This presentation is intended for information and discussion purposes only and does not constitute legal or professional investment advice. Statements of fact and opinions expressed are those of the participants individually and, unless expressly stated to the contrary, are not the opinion or position of Harbor View Advisors, LLC (“HVA”). The information in this presentation was compiled from sources believed to be reliable for informational purposes only. HVA does not endorse or approve, and assumes no responsibility for, the content, accuracy or completeness of the information presented.