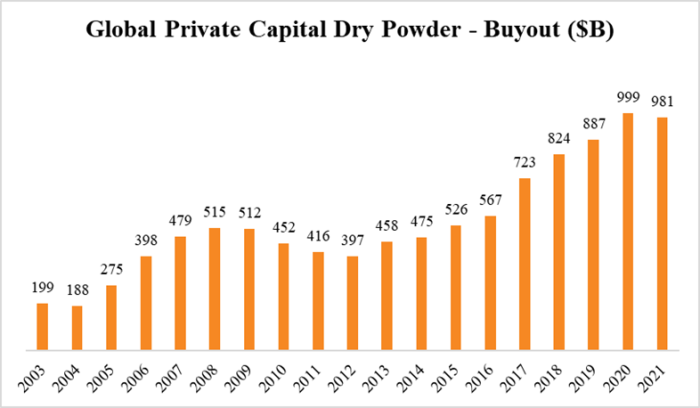

Inflation is at levels not seen in four decades, interest rates are rising and the public equity markets have officially entered bear market territory. At the same time, the private capital market remains flush with capital, having just wrapped up yet another record fundraising year. In fact, since 2000, Global Private Capital assets under management have grown from $700 billion to $5.3 trillion as of year-end 2021. Dry powder in buyout funds stands at $981 billion, just shy of the record level reached in 2020. There is still a lot of capital to be put to work.

What do these crosscurrents mean for the M&A market? For business owners considering a sale, what are the implications of the tug of war between negative macro trends and a significant PE war chest of cash that must be deployed?

First, let’s look at where things stand and how we got here…

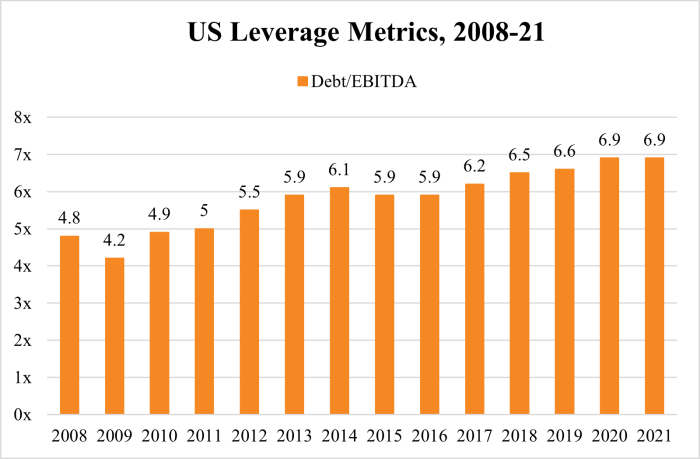

For two decades, private equity buyers have been able to take advantage of cheap and plentiful debt. Buyout leverage has risen from just over 4x in the wake of the financial crisis to nearly 7x.

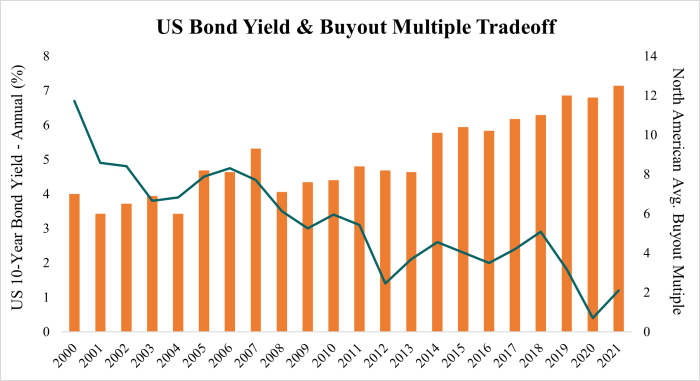

The long slide in interest rates and the avalanche of PE fund flows have fueled an increase in valuations and deal activity. In 2021, private equity buyout volumes reached $1.1 trillion across 4,300 transactions. The dollar figure represents a first-time breach of $1 trillion, far eclipsing any previous year, and more than double the 2020 total. Since 2000, average multiples for North American buyouts have risen from less than 7x to over 12x.

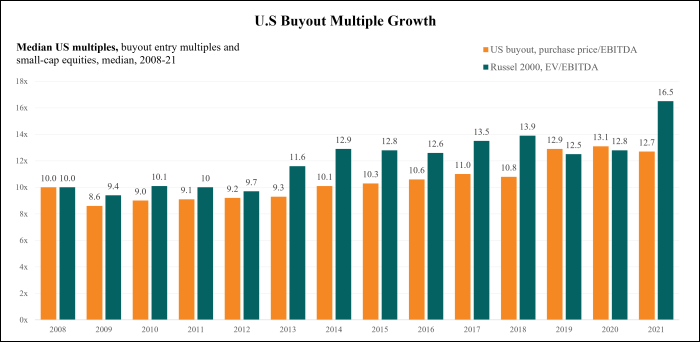

However, since 2019, median M&A valuations have held steady at 12.5-13.0x EBITDA, while small-cap public equities saw a sharp increase in value, with the Russell 2000 valuations spiking nearly 30% in 2021.

As we consider the landscape in 2022, the first quarter saw healthy M&A volumes, albeit somewhat below the torrid deal-making pace set in 2021. So far in Q2, buyer activity suggests that there is still strong motivation to deploy capital, but buyers are mindful of the uncertainty that lies ahead.

Looking ahead…

Given the much sharper increase in public valuations, it seems fair to conclude that the public equity markets were primed for a sharper pull back than private market M&A multiples. Secular trends that have fueled M&A transaction activity remain in place, including the need for generational business transfer and the opportunity to invest in transformative technology innovation and efficiency. Interest rates can increase significantly and still be moderate by historical standards. Cash in corporate and private equity coffers remains plentiful.

Our expectation is that we will still see healthy deal volumes for the 2022-year.

Beyond 2022, a lot will depend on the Fed’s ability to engineer the allusive soft landing. If interest rates settle at a level above current rates, but still moderate in historical terms, deal volumes could continue to be reasonably healthy - but at more modest valuation levels. If taming inflation necessitates a steep rise in interest rates leading to a tough recession, the deal market will be in for a bumpy ride. It is worth noting that the current Wall Street consensus is for a mild recession in 2023.

In either case, it would be prudent for prospective sellers to temper valuation expectations. Higher interest rates, growing uncertainty and the prospect of persistent inflation, recession or (worst of all) stagflation, will almost certainly weigh on valuations. One thing seems clear – we will likely look back on 2021 as a peak in the deal market. However, significant cash levels and the need for generational business transfer should also provide something of a floor for deal volumes and valuations alike.

Sources:

DISCLAIMER This presentation is intended for information and discussion purposes only and does not constitute legal or professional investment advice. Statements of fact and opinions expressed are those of the participants individually and, unless expressly stated to the contrary, are not the opinion or position of Harbor View Advisors, LLC (“HVA”). The information in this presentation was compiled from sources believed to be reliable for informational purposes only. HVA does not endorse or approve, and assumes no responsibility for, the content, accuracy or completeness of the information presented.