We may be seeing an M&A renaissance in FinTech & Business Services, particularly in more sluggish areas such as MortgageTech. Given recent observations, we are guiding our clients to take a page from the playbook of prior cycles: Get started EARLY in a macro turn.

Case in point:

Four observations over the past few weeks suggest M&A activity is picking up:

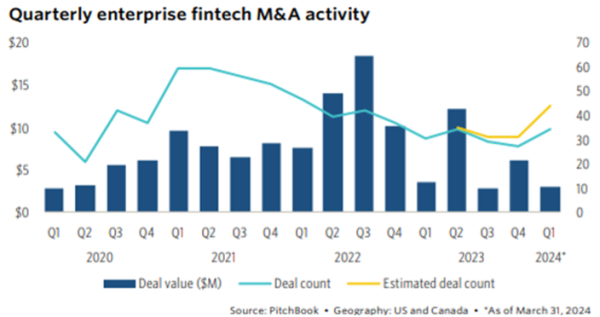

1. Transactions are on the rise: PitchBook called it a Private Equity “comeback” in Q1 with enterprise Fintech M&A transactions up 50% YoY. The strongest M&A activity is in payments, the “CFO stack”, capital markets and infrastructure, particularly software solutions. The graph below presents the last 4 years of quarterly performance, with the recent upturn in Q1 of 2024.

2. Financial sponsors are first-movers, with corporates lagging: PE buyout and VC investment activity is healthy while Corporate Development Teams have been more cautious – with an exception of larger deals like Capital One/Discover ($30+B), Nasdaq/Adenza ($10.5B) and possibly Amadeus IT Group or Fiserv hunting Shift4 (likely in the $5.0B range).

3. Valuations favor the brawny – however, trends are shifting: Consistent with our prior market commentary, premiums are most correlated with earnings quality, outlook and investor need. Size matters and has been the dominant driver of transaction multiple expansion, however, industry commentary suggests future M&A value creation will require more savvy operators. The PE model is shifting from valuation arbitrage and scale benefits of the traditional “platform+buy+buy” method to more of a “buy/build” model that is dependent on integration, organic growth, and operating leverage.

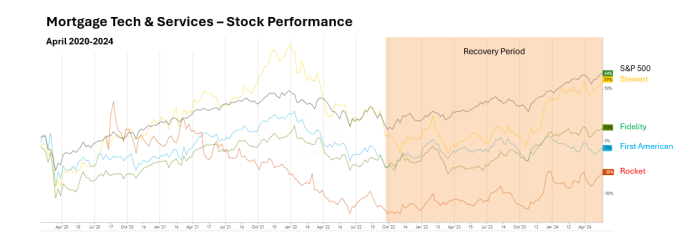

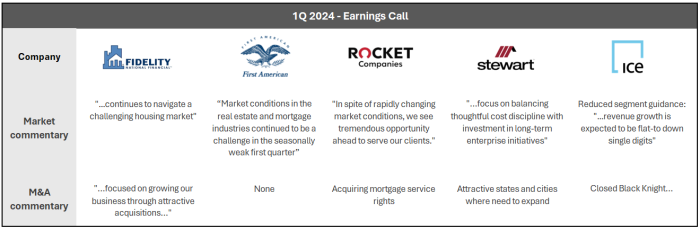

4. MortgageTech & Services is beginning to recover: Mortgage is the most cyclical niche within the FinTech market and as the first graph below suggests, the leading MortgageTech stocks have been underperforming. However, as end markets and interest rate visibility stabilizes, the stocks are on a recovery. Although the commentary from 1Q earnings calls suggests unsettled market conditions, there is some M&A activity, captured in the second graphic below. The marquee transaction was the Intercontinental Exchange (NYSE: ICE) $11.9B acquisition of Black Knight. Other noteworthy, but smaller deals include multiple small title company acquisitions by First American and Stewart, a $150M investment in Blend (NYSE: BLND, $790M market cap) and Doma’s (NYSE: DOMA) $85M go-private.

The bottom line – the FinTech M&A market seems to be stronger than investors realize as perhaps even the weakest niche of Mortgage is beginning to show signs of new life.

Connect with our team to learn more about what he’s hearing and seeing in the space.

Sources:

DISCLAIMER This presentation is intended for information and discussion purposes only and does not constitute legal or professional investment advice. Statements of fact and opinions expressed are those of the participants individually and, unless expressly stated to the contrary, are not the opinion or position of Harbor View Advisors, LLC (“HVA”). The information in this presentation was compiled from sources believed to be reliable for informational purposes only. HVA does not endorse or approve, and assumes no responsibility for, the content, accuracy or completeness of the information presented.