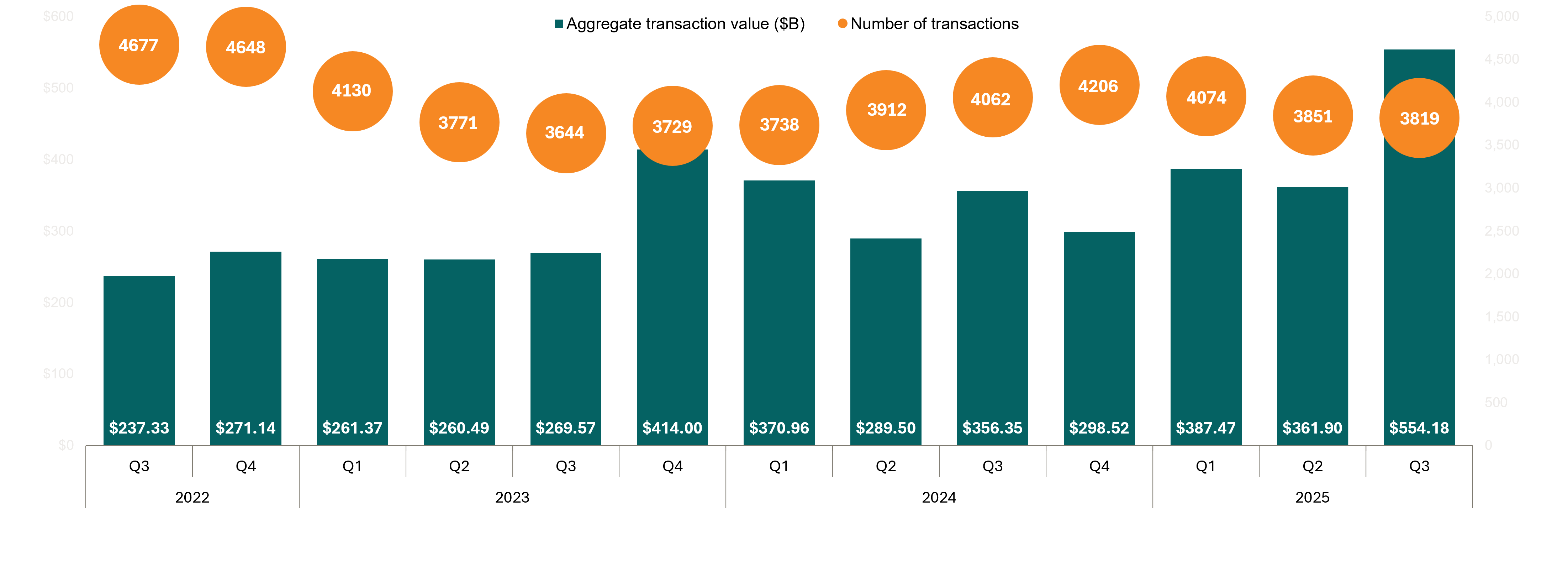

It seems the M&A market is gaining momentum into year-end – perhaps even stronger than where we were before foreign trade complications pulled the rug out from under most founder and investor plans. Recent client and market commentary suggests a corner has been turned on deal expectations, with notable headline comments like “Animal Spirits have returned in the M&A market…”1. Notably, S&P tracking of U.S. M&A deals indicates the activity remains steady, although value is at the highest point since 2021 with several mega-deals in the 3Q of 20252.

3Q US M&A Value Highest Since 2021

*Chart redesigned and data pulled from S&P Global “M&A in Focus: The State of the Middle Market” webinar presentation slides

We highlight three perspectives below:

Current M&A Transaction Market Commentary:

Buyers are cautiously optimistic as deal flow improves. Reported M&A transaction volumes remain down vs last year (down 12% YoY for transactions less than $250M in Enterprise Value). Yet, origination intensity is rising as investors note a marked improvement in deal flow and quality at the beginning of Q3.

A cross current of forces is driving competition for acquisitions. Solid companies command strong valuations given thin supply, benefitting from scarcity value amid investor sense of urgency. Investors are employing continuation vehicles as portfolio companies improve performance with a priority on M&A.

Valuation tailwinds set the stage for 2026. Overall, market multiples which remained steady through 2025 saw a slight uptick in Q3. Smaller transactions, under $100 EV, have seen an average trading range of 6.3-8.0X EV/EBITDA3 but can vary widely across industries and business models. Notably, higher quality assets command 1-2X turn premium over industry peers.

HVA Client End Market Commentary:

Human Capital Management – Recruiting and talent acquisition can be early indicators for the labor market and related growth and investment. Several market participants have noted signs of a pick-up in hiring activity.

Technology Services – Views from the Cyber Security and Managed Services world point to a vibrant recovery from the malaise of earlier this year – “The spigots of IT and Cyber spend are back on, and on strong.”

Staffing – Another niche market that has historically led a rally, as employers action up on a turn with temporary staff first – we are hearing some positive comments about activity – a notable relief from the doldrums of the past two years.

A View from BOTH the Sell-side and the Buy-side:

Our buy-side activity is strong, with Private Equity clients engaging both platform and addon efforts across a wide range of niche markets, including Data Center Build, Managed Security Services Provider (MSSP), Accounting and Legal Services, Proprietary Data Services, Insurance Claim Investigations, Title Insurance Agents, Environmental Services, and Facility Services.

Sell-side engagements and pitch activity are picking up into year-end pointing to a stronger first half of 2026. Founder confidence is rising, having cut through market challenges, including:

Adjusting to dramatic alterations Google is implementing with AI;

Clarity around tariff terms and impacts; and

Improving outlook for cyclical markets like MortgageTech.

Nothing speaks louder than a closing! In the tough and competitive electrical contractor arena, we closed on a great outcome for our client, the Hinson family, along with their wonderful management team at James D. Hinson Electrical Contracting.

Sources:

1 Kevin Foley, JPMorgan's global head of capital markets, October 8, 2025.

DISCLAIMER This presentation is intended for information and discussion purposes only and does not constitute legal or professional investment advice. Statements of fact and opinions expressed are those of the participants individually and, unless expressly stated to the contrary, are not the opinion or position of Harbor View Advisors, LLC (“HVA”). The information in this presentation was compiled from sources believed to be reliable for informational purposes only. HVA does not endorse or approve, and assumes no responsibility for, the content, accuracy or completeness of the information presented.