We believe the challenges of the past nine months have created a buildup of kinetic energy in the M&A market, particularly for technology. We have worked with our clients across a spectrum of outcomes, and the most enduring trend we have witnessed is that resiliency is now an elevated attribute in the “new normal” due diligence. The sellers with the most durable business models are powering through their sell-side processes. On the buy-side, the private equity backed strategics have stepped up their add-on efforts. We expect to see rising deal volumes in 2021 (thankfully only a few months away). We see dealmakers gaining confidence, still wary of the adverse selection of non-performers or the fire-sale-chasers, the focus has shifted to getting good deals done.

In this note, we consider what is getting done, who is powering the resurgence into the close of a crazy 2020 and what the next twelve months of Technology M&A could look like.

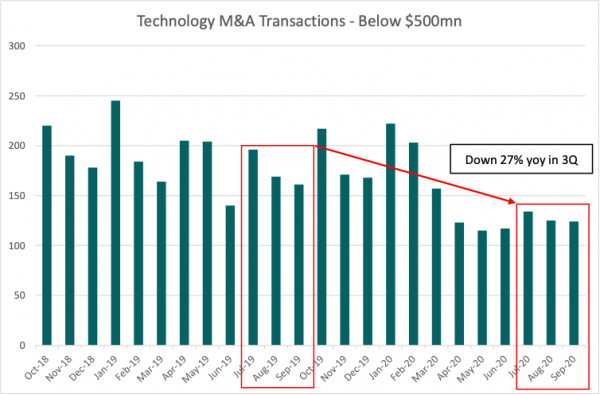

First, let’s take a look at what is closing. In round numbers, excluding the mega deals, the middle of the fairway in the US Technology & Services market includes about 2,000+ transactions a year. This year started off well and held up through the first quarter with 580 transactions (about even with 2019), before the wheels started coming off. In the second quarter the number of deal closings were down by 35% year over year. Still, some deals were getting done – which is notable. What could have been an M&A summer of deep despair, became more of a hunker down story. The decline in deal volume has slowed a bit, with 3Q down only 27% yoy and so far, September is on track for 125 transactions, including one of our clients in the Azure cloud platform space (congratulations to Brian Knight and the Pragmatic Works team!), check out the announcement here. It would seem, the M&A market may not be getting any worse, and we are seeing certain niche markets within software and tech-enabled services regain their footing.

Source: Pitchbook – 2019-2020, Below $500mn EV, US Technology & Software only

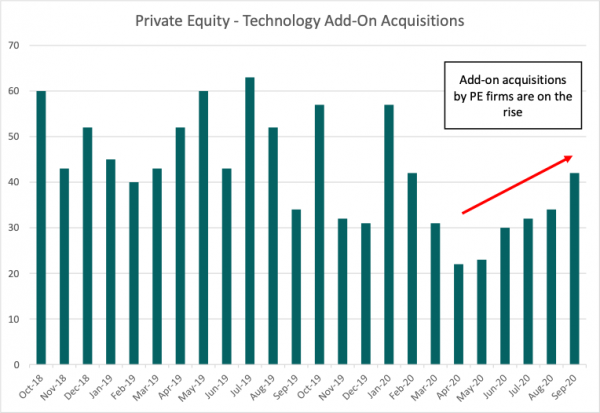

Second, who is powering this resurgence in activity? We followed the money and not surprisingly, Private Equity firms are seeking to take advantage. After a short retrenchment during March/April when portfolio company lines were drawn down, cash hoarded and the sleepless nights of end-market worry, the PE firms are now hard at work. We published a note in June about how “Active Acquirers” through prior downturns achieved roughly 3X the shareholder return for their investments. Through our buy-side work, we have seen first-hand how PE-backed firms, with a now COVID tested investment thesis are pursuing add-ons with gusto. Add-on acquisitions are down with the overall M&A trends; however, deals have risen month over month since April and so far in September add-ons represent 82% of all PE transactions, the highest proportion in the past two years.

Source: Pitchbook – 2019-2020, Below $500mn EV, US Technology & Software, Private Equity only

Finally, and most importantly, what does this mean for the future of Technology M&A? We are optimistic based on three inputs:

References:

DISCLAIMER This presentation is intended for information and discussion purposes only and does not constitute legal or professional investment advice. Statements of fact and opinions expressed are those of the participants individually and, unless expressly stated to the contrary, are not the opinion or position of Harbor View Advisors, LLC (“HVA”). The information in this presentation was compiled from sources believed to be reliable for informational purposes only. HVA does not endorse or approve, and assumes no responsibility for, the content, accuracy or completeness of the information presented.